Dr Carole Nakhle

Today’s relatively low price of oil seems to have reconciled the otherwise conflicting interests of the world’s largest producers and consumers. Organizations representing these two groups have warned of negative repercussions, including a price spike that could follow from lower investment. However, the relationship between oil prices, investment and future supply is not so straightforward.

Though they usually represent opposing interests, the Organization of Petroleum Exporting Countries (OPEC) and the International Energy Agency (IEA) are both concerned about cheap oil. They have warned that the drop has led to a significant reduction in investment and is therefore planting the seeds of a tighter market and potentially higher prices in the medium to long term. OPEC currently supplies more than 41 percent of the world’s oil, while the IEA includes 29 net oil importers – all members of the Organisation for Economic Co-operation and Development (OECD), a group of the world’s richest countries.

Abdalla Salem El-Badri, OPEC’s secretary-general, has made it clear that lower investment will result in reduced supply in the near future. That could mean prices climbing as high as $200 per barrel. By the same token, Fatih Birol, the IEA’s executive director, cautioned, “Now is not the time to relax. Quite the opposite: a period of low oil prices is the moment to reinforce our capacity to deal with future energy security threats.”

These concerns are legitimate. The oil price is a powerful factor that determines short-term investment. This, in turn, shapes long-term supply. Investment in oil and gas – from exploration to the development and maintenance of fields – is needed to increase production and satisfy market needs. Lower oil prices discourage investment spending, resulting in the delay or cancellation of projects and thereby reducing potential future supplies. Ali al-Naimi, the Saudi oil minister, has said the world needs some $700 billion in investment over the next decade to meet global oil demand, which is expected to increase by at least one million barrels a day annually.

Nevertheless, a closer look at past trends shows that the relationship between oil prices, investment and supply is not always so clear-cut. Other factors sometimes come into play, distorting the relationship. Studies of the correlation between investment and the prices have not conclusively found a causal relationship.

Investment drop

According to the IEA, capital investment in the oil and gas sector declined by 20 percent last year. The trend is expected to continue throughout 2016. If it does, it will be the first time in 30 years that the industry has witnessed two consecutive years of declining investment. This has serious long-term implications.

The steep drop is not a complete surprise, given the capital spending that preceded it. Annual investment in the oil and gas industry increased by 50 percent between 2009 and 2014, to $890 billion, according to a survey by the consulting firm Deloitte.

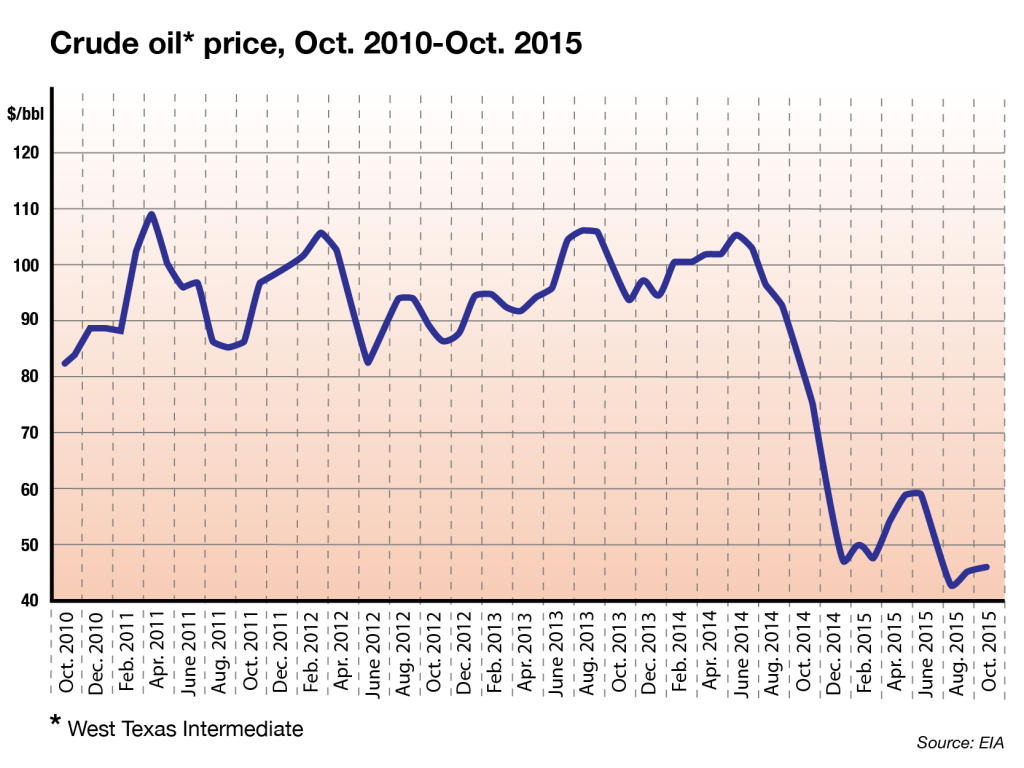

Besides, the investment cuts cannot be solely explained by the fall in oil prices since their peak between 2011 and summer 2014, when they hovered around $100 a barrel. Some major oil companies began reducing investment before oil prices started their decline. As early as July 2013, Total announced that it would reduce capital expenditures in 2014. In March 2014, Exxon Mobil said it would cut back its investment spending from $42.5 billion to $37 billion in 2015-2017, and revised its production target downwards.

Usually, the perception is that higher prices translate into higher profitability for the oil companies. In reality, the shares of international oil companies during the high-price period underperformed the broader equity market. Returns did not increase as had originally been expected. According to the energy research firm Douglas-Westwood, the combined cash return on capital invested by the so-called global “supermajors” – ExxonMobil, Royal Dutch Shell and BP – had reached its lowest level in 40 years at the end of 2013. And in January 2014, Shell issued its first profit warning in a decade.

Cost and effect

Chevron’s Chief Executive Officer John Watson explained this seemingly contradictory outcome best when he said, “Essentially, for a company like mine and many others, $100 a barrel is becoming the new $20 in our business.”

According to a five-year survey carried out by the risk management company DNV GL, industry firms repeatedly identified rising costs, skill shortages and increasing regulations as the industry’s top three barriers to growth. These all predated the fall in the oil price.

One frequently overlooked factor is how sensitive upstream costs are to the oil price. Upstream costs rise when oil prices rise, typically with a lag of six to nine months. When oil prices are high, companies are in the mood to spend. But given the limited pool of equipment (including rigs) and workforce (such as skilled engineers and project managers) an increase in activity pushes up labor buy generic accutane uk costs and rig day rates (the amount a contractor gets paid for a day of operating a drilling rig). The opposite is true when prices fall.

If the oil price increases faster than costs do, as it did prior to 2011, the increased outlays can be offset. However, between 2011 and summer 2014, costs continued their rapid rise, while the price of oil held steady. Net returns in the industry shrank.

The drop in oil prices is expected to put downward pressure on costs. In the United Kingdom, for instance, the industry expects the average operating cost per barrel of oil equivalent to fall from £17.80 ($26.50) in 2014 to £15 ($22.30) in 2016, reversing a three-year trend.

Government’s role

The effect of government policy also cannot be overstated. In its annual activity report on the UK Continental Shelf, Oil & Gas UK, an industry association, did not see the drop in oil prices as the root of the problem facing the sector. High costs, high taxes and an under-resourced regulator were found to be the real challenges.

Back in the early 1990s, the U.S. portion of the Gulf of Mexico was considered a dead sea when it came to exploration. In an attempt to reverse that perception, the government introduced new fiscal incentives through the Deep Water Royalty Relief Act of 1995. Despite the relatively low oil prices at the time, the region witnessed a remarkable jump in leases for deepwater fields – from 171 in 1995 to a record high of 1,110 in 1997. A total of 3,000 deepwater lease bids were made between 1996 and 1999, and deepwater oil production increased from 42 million barrels in 1994 to 348 million barrels in 2004.

Mexican example

More recently, Mexico held bidding rounds, the first in 75 years, to license oil and gas contracts in the Gulf of Mexico to international companies. The first auction, held in July 2015, was described as a failure since its results were well below the government’s expectations: only two of 14 shallow-water exploration blocks were awarded, and the winning consortium did not include a major oil company. Crude oil was priced just under $55 a barrel at the time.

Ahead of the second round, the government adjusted the bidding terms to make them more attractive and clarified some contractual ambiguities. The September 2015 auction yielded a better outcome. Three of the five shallow-water production blocks on offer were awarded, one of them involving a contract with the Italian major Eni. The oil price had fallen to about $46.

The combination of improved terms and less risky ventures (since the first auction focused on exploration while the second auction on production) seemed to have more than compensated for the lower oil price.

Wild card

The traditional discussion of price, investment and supply takes into account the long lead time between making the initial investment and bringing the first production onstream. For conventional oil, this can take years and in some cases more than a decade. So today’s conventional oil production is the result of exploration carried out more than a decade ago and investment decisions made more than five years ago.

With shale oil, however, the investment cycle is much shorter and the lead time has shrunk to months. This is partly due to the technology involved in these operations and partly due to the nature of companies working in this sector. Such firms are small, highly leveraged and able to adapt more easily to changing market conditions than the multinational behemoths dominating the conventional oil business. Given its flexibility, shale production is perhaps the biggest unknown in the future development of the global oil market.

This suggests that current prices will have little impact on existing production from conventional oil fields. Shale oil production will be more responsive, but the pace of its decline will depend on cost efficiency improvements, which so far have been remarkable. Once oil prices start to recover, the speed with which shale oil supply rebounds will be an even more interesting development to watch.

Forecasting oil prices and future investment is not a straightforward exercise. It may well be that investment cutbacks being made now will lead to tighter supplies in the longer term. If one assumes high demand for oil, the result would be a spike in prices.

Nevertheless, other variables such as costs, government policies and technology could offset these pressures by increasing the efficiency of investments. Demand plays an equally important role and is highly unpredictable. All these factors should be taken into account when considering the future of the global oil market. Additionally, the exploitation of shale resources has introduced a new dynamic that may require us to think about the market in a different way.

Article Reproduced with the kind permission of Geopolitical Intelligence Services

Related Comments

“The complex relationship between oil price and investment, and the impact on future supplies”, Dr Nakhle, Apr 2016