In an interview given to Azeri.Today, Dr Carole Nakhle, CEO of Crystol Energy, discusses Trump’s energy policy, oil price, the EU’s dependence on Russian gas as well as Azerbaijan’s potential in the EU’s gas supply.

Q: What are your expectations of Trump’s new energy program? How will this program influence the economy of Russia and the countries of the post-Soviet oil and gas producing countries?

A: President’s Trump energy program is still unfolding but from what we have seen so far, he is sticking to the pledges he made during his presidential campaign.

In this respect, he comes across as a friend to the US oil and gas industry both locally and internationally. Domestically, his energy program aims mainly at relaxing the regulatory burden which was tightened under the Obama Administration, on both producers and consumers. However, his policies will result in two opposing effects in terms of impact on oil prices: A lowered regulatory burden on producers (e.g. the executive order on easing regulations on offshore and onshore drilling — particularly offshore Alaska) will support domestic supply growth (so downward pressure on price) and a lowered regulatory burden on the demand side (e.g. relaxation of the CAFE – car fuel efficiency – standards) will encourage local demand (so upward pressure on price). The same effect is true internationally: increase supply by offering international companies to do more in the US and demand by abandoning Paris climate change deal.

The speed at which the impact of such changes will become more notable will depend on the speed at which President Trump can implement the above policies which can take a while to materialise.

That said, the recent impressive growth in US oil and gas production – whether from conventional oil and gas (primarily the US Gulf of Mexico) or unconventional/ shale, has been the result of the industry’s reaction to the international price of oil. For instance, the record increase expected this year from the US Gulf of Mexico is the outcome of investment decisions taken when the oil price was hovering above US $100 per barrel between 2011 and 2014.

Shale production is more responsive to current oil prices creating a major challenge to OPEC and its coalition of non-OPEC producers which is led by Russia. The ability of US shale producers to react relatively quickly to changes in prices has constrained the effectiveness of production cuts from OPEC and its allies.

And it is not just oil. The US, which is traditionally a gas importer, is expected to become a net gas exporter by 2018 also thanks to the shale revolution which kicked off at the end of the last decade. As the US joins the international club of gas exporters, it will simply create additional competition to established and new gas producers.

To summarise, the effects of President Trump’s energy program will be more visible in the mid-term, should he succeeds in fully implementing the relaxation of oil and gas regulations. In the long term, if his pledge to withdraw from the Paris climate change agreement is fully adopted, he will provide a further boost to the US oil and gas (as well as coal) industry. How will that translate on the global oil scene will depend on several factors mainly production performance outside the US and global demand growth, given the plain fact that oil market is global.

Q: As you know, Europe depends heavily on Russian gas. Do you think that European countries can overcome the dependence of Russian gas?

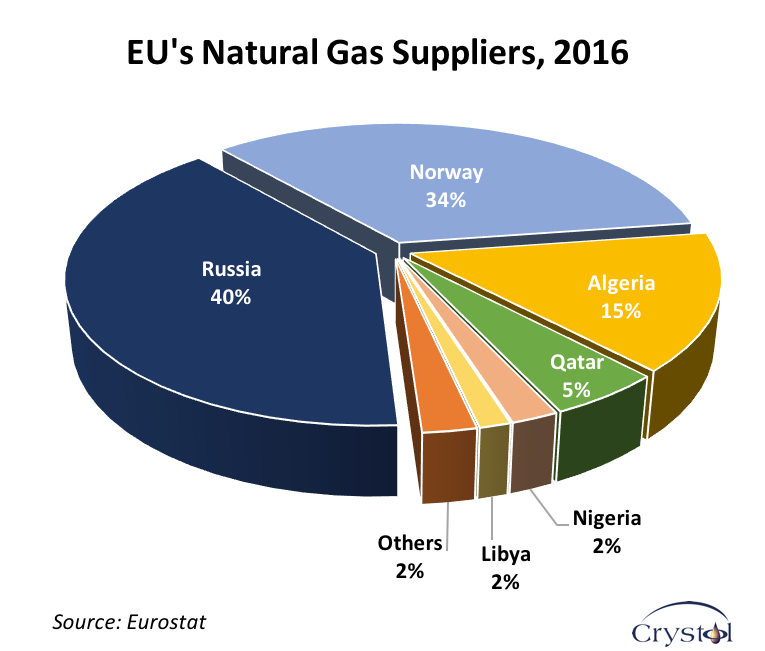

A: It is worth first noting that Russian gas dependence is not evenly distributed among the EU members. Most European countries in the east depend 100 per cent on Russian gas supplies; others in the west hardly at all.

Overall, the EU is in a better state than it was 20 years ago, partly because it has succeeded to diversify its gas supplies and partly because gas markets are undergoing structural changes potentially benefiting buyers.

Russia has been a major supplier of gas to Europe for decades. However, the EU’s dependence on Russian gas has been declining since the 1990s, as Europe maintains its march to diversify its sources of gas supplies. More than 75 percent of the growth in EU gas imports now originates from countries other than Russia. In addition to Russia, the EU has been relying on imports from Norway (primarily pipeline) and North Africa (mainly Algeria) and the Middle East (largely Qatar) with LNG increasingly more popular.

New suppliers may well emerge in the coming years; in the short term the US is a real contender and in the longer term, new gas may start to flow from Eastern Mediterranean to Europe, although that depends on development plans for gas finds in that politically divided region. And, of course, there is the increasing potential from Central Asia especially if the Caspian countries sign the Convention of the Caspian Sea which in turn will facilitate the development of the necessary infrastructure to strengthen the connection between the region and Europe.

Meanwhile, as renewable energy continues its rapid growth momentum in the EU, there will be a greater demand for baseload power specially to address the intermittent nature of renewables. To some extent this has been satisfied with coal (shipped cheaply from the US where it has been replaced by cheaper shale gas). If the EU wants to effectively limit CO2 emissions, it should use more gas and/or nuclear. Natural gas is the transition fuel to a cleaner and greener future as it emits less CO2 than coal or oil.

Q: Oil prices are currently in the range of 50-60 dollars per barrel. What is your forecast for oil prices for the coming years?

A: There are several moving parts – some in opposing directions, that will shape the global oil market and therefore the oil price. In this respect, predicting the oil price is fraught with a high degree of uncertainty. Oil price volatility has been an inherent business risk since the inception of the industry more than a century ago and this is unlikely to change.

What we know with greater certainty, however, is that the oil market has changed fundamentally particularly on the supply side.

The advent of shale has brought in a more flexible supply that is more responsive to changes in prices – unlike conventional oil where a long lead time between development and first production is the norm. OPEC succeeded to put a floor under prices. But there is also a price ceiling, determined primarily by shale oil’s capacity to increase production in response to higher prices (plus its ability to hedge in financial markets), in addition to record high inventories. On the demand side, we are seeing a structural decline in OECD demand for oil.

Q: What can be Azerbaijan’s role in the gas supply of European countries? What will the construction of TANAP Europe bring?

A: The Caspian in general and Azerbaijan in particular have been on the EU’s top list of region/countries to diversify gas supply routes, mainly through the EU’s fourth, Southern corridor, which would bring natural gas from the Caspian region, the Middle East and East Mediterranean basin (the other corridors being: the Eastern corridor (Russia); Northern corridor (Norway) and Western corridor (North Africa)).

The Southern gas corridor was described by the European Commission as one of the EU’s highest energy security priorities. Several pipeline options are being considered, as part of this corridor. The TANAP is one of them but it has much better chance of bringing gas to Europe from Azerbaijan’s Shah Deniz-2 gas field, and other areas of the Caspian Sea, mainly to Turkey than other projects that have been considered. According to the project’s partners, the initial capacity will be 16 billion cubic meters (bcm) per year which will be gradually increased to 24 then 31 bcm, the equivalent of between 4-8 percent of total EU gas consumption, further supporting the EU’s efforts to diversify its gas supplies and achieving a greater security of supply.

The interview was originally published on Azeri.Today and is also available in Russian.