Dr Carole Nakhle

Saudi Arabia is once again keeping analysts busy worldwide. This time attention has been drawn by an audacious economic reform rather than by oil policy, although the two are closely intertwined. Some of the development strategy’s goals are not new and others are probably unattainable, but there seems to be a stronger will to proceed today than in the past decades. The journey will not be quick, easy or cheap. In the short term, Riyadh’s new policies will have limited implications on the oil market.

In April 2016, Saudi Arabia published its first long-term reform plan, “Vision 2030,” which presents a roadmap for the kingdom’s economic and social policies. The media has described this document as the biggest economic shake-up since the establishment of Saudi Arabia.

The publication was preceded by McKinsey & Company’s report “Saudi Arabia beyond oil: The investment and productivity transformation” in December 2015. This study closely corresponds with “Vision 2030,” only with less detail and fewer numbers. McKinsey & Co. is one of the consultants that advised the Saudi government on its reform. Deputy Crown Prince Mohammed bin Salman also previewed some of the Vision’s main points in various interviews to international media outlets ahead of the official publication date.

In publishing the “Vision 2030” strategy, Saudi Arabia fell in line with what used to be fashionable in its neighborhood. Bahrain, Qatar, Kuwait and the United Arab Emirates had all announced their own versions of Vision 2030, only six to nine years earlier. The need and desire to diversify away from oil lay at the heart of all these documents, just as it does now in the case of Saudi Arabia.

The Saudi “Vision 2030” is a fairly general document. More details were provided in a National Transformation Plan (NTP) released in June. The NTP is the first of a series of executive programs that will address certain aspects of the reforms. It is also the kingdom’s tenth five-year plan, maintaining a tradition dating back to the First Development Plan in 1970.

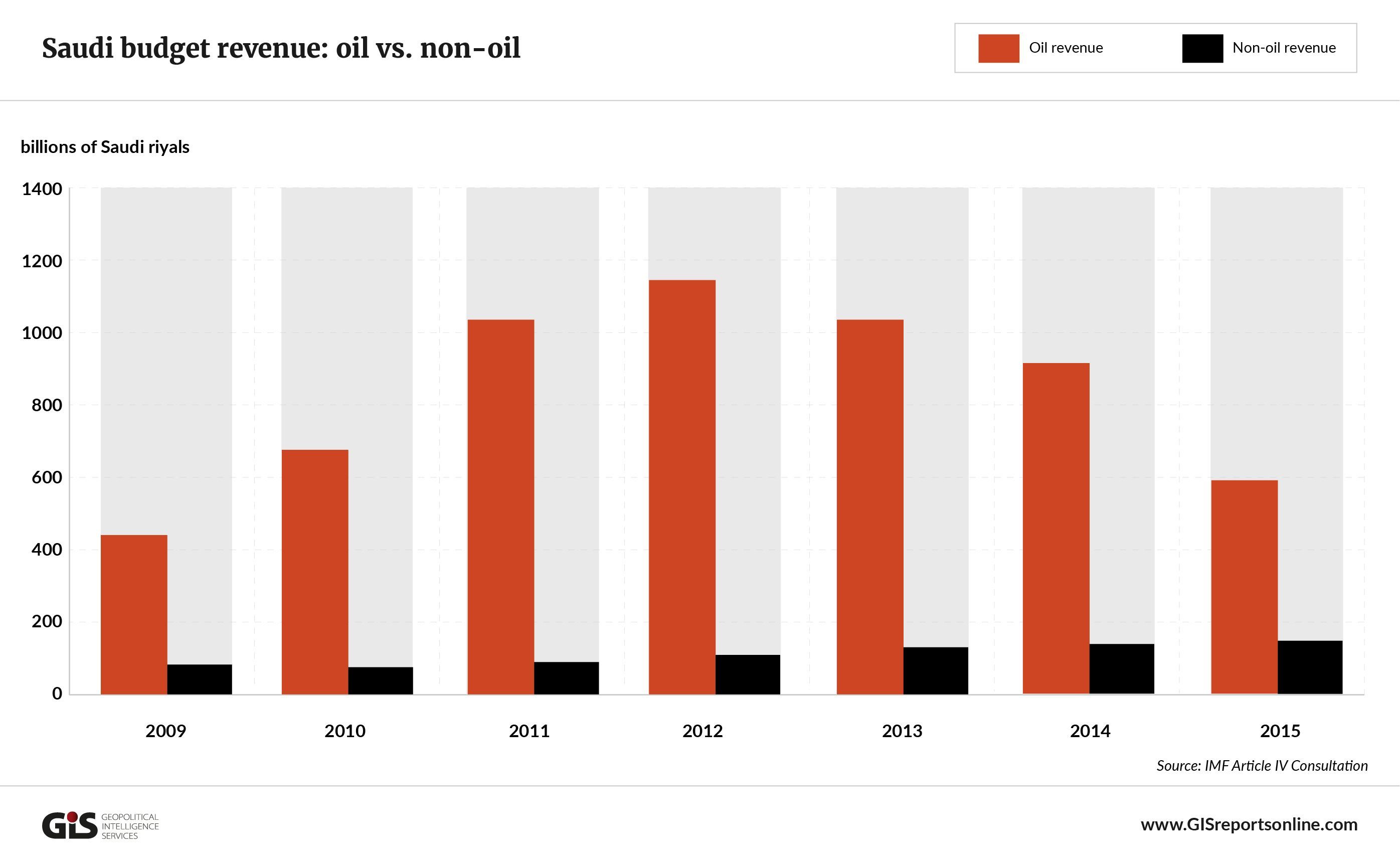

The NTP sets specific targets for 24 ministries and government agencies to promote social and economic goals. The latter chiefly focus on balancing the budget, creating jobs, reducing subsidies, diversifying the economy and developing the private sector. Other aims include improving transparency, efficiency and productivity. In all, the document enumerates a total of 543 reforms with a price tag of 268 billion Saudi riyals ($78 billion).

For instance, one of the goals for the Ministry of Finance is to increase non-oil revenue more than threefold to 530 billion riyals in 2020. Over the same period, the Ministry of Energy, Industry and Mineral Resources is expected to increase the value of non-oil commodities exports from 185 billion riyals to 330 billion.

Deja vu?

A cynic would argue that the Saudi economic blueprint contains few novel ideas. Nonetheless, the goals it proclaims are probably the most sweeping of any attempted in the Middle East or by an oil-producing developing country.

The need for bold measures to achieve greater economic diversification, reduce dependence on oil revenue and establish a more sustainable growth model has been discussed in Saudi Arabia for decades and has been long promoted by organizations such as the International Monetary Fund and the World Bank.

The introduction of a Value Added Tax (VAT) to diversify the government’s revenue base, along with other new “sin” taxes such as a levy on sugary drinks, was considered in the 1990s. The potential application of an income tax on non-Saudis, as highlighted in the NTP, brings back memories of the income tax that applied in Saudi Arabia between 1970 and 1975, and also the government’s failed attempt to reintroduce such a tax on expats in 1988.

Experience shows that such reformist ambitions tend to resonate strongly during periods of low oil prices, before their urgency fades away when oil prices increase. This time, however, Saudi Arabia seems more determined than ever to carry out a landmark transition, and the whole world is watching.

Reform triggers

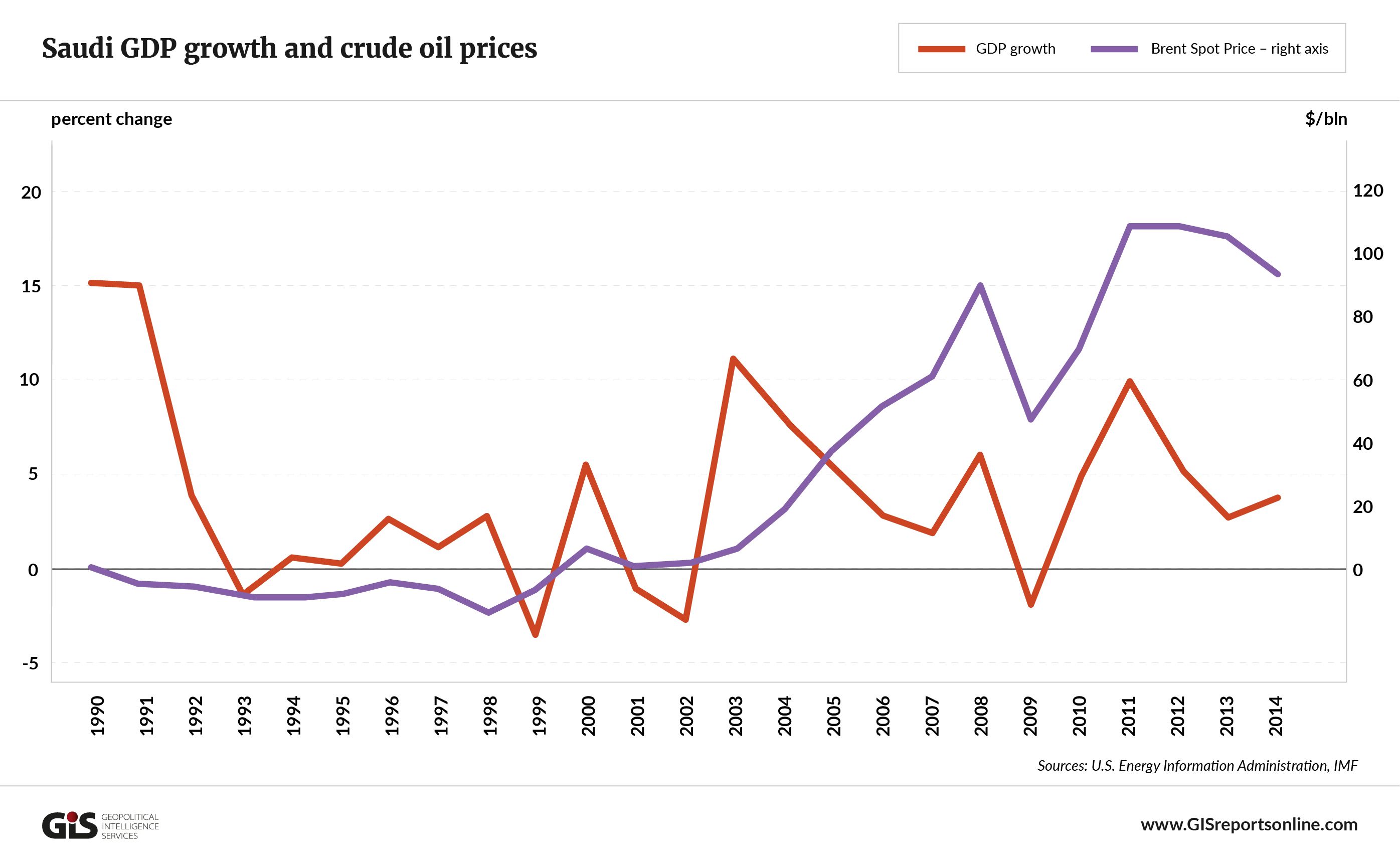

Oil price volatility has been the traditional troublemaker. Over time, however, new problems have emerged and their imprint is visible in the Saudi reform strategy.

First, oil producers starting with Saudi Arabia are facing the challenge of climate change. While this is more of a long-term issue, there is a clear global trend toward phasing out fossil fuels, which eventually could leave the world’s second largest holder of proven oil reserves (after Venezuela) with a redundant resource.

The other, more pressing concern is demographic. Saudi Arabia needs to create a more vibrant job market for its rapidly growing working-age population. Vision 2030’s first “pillar” and possibly most urgent priority is to create a “vibrant society” that will engage educated young people. Several of the strategy’s aims are carefully engineered to appeal to the aspiring younger generation, thereby strengthening the social contract between rulers and ruled. The second and third pillars of Vision 2030 are a “thriving economy” and an “ambitious nation.”

While the oil sector is a relatively large employer, it is a capital-intensive industry and job opportunities are constrained. The Saudi public sector is already bloated and suffers from inefficiencies. The new jobs, therefore, must come from the private sector.

McKinsey estimates that to double its gross domestic product and create as many as 6 million jobs by 2030, Saudi Arabia would require about $4 trillion in investment in the non-oil sector, primarily from private sources. The plan is for eight industries – mining and metals, petrochemicals, manufacturing, retail and wholesale trade, tourism and hospitality, health care, finance and construction – to generate more than 60 percent of the country’s economic growth. The NTP is an initial step toward achieving that goal, as it seeks to create more than 450,000 jobs in the nongovernment sector by 2020.

Saudi Aramco

Perhaps the most striking reform proposal is for an initial public offering of the national oil company. Saudi Aramco is the world’s largest oil producer and most influential oil company in the world, supplying more than 13 percent of global demand. It is also the cornerstone of the Saudi economy.

The announcement of Saudi Aramco’s IPO came as a surprise. While some oil producers have publicly listed their national oil companies, their upstream oil sectors tend to be already open to private investment. Saudi Arabia, on the other hand, is one of the very few countries that remain closed to upstream private companies. This led some analysts to predict that the IPO would be limited to Aramco’s downstream assets, such as refineries.

According to Prince Mohammed bin Salman, however, “the mother company will be offered to the public as well as a number of its subsidiaries.” The share sale would give investors a stake in the world’s largest oil fields and also make public Aramco’s financial accounts, subjecting the company to greater scrutiny. While this is a welcome move, it may cause some backlash if the published data is not in line with expectations.

One wonders why the government chose this option instead of simply opening the sector to international oil companies, as is the common 21st century practice. Mexico went down that route two years ago, after 75 years of being closed to private investment.

An IPO would likely generate faster revenue, improve transparency and support Saudi Aramco’s international expansion. However, allowing the internationals in would still let Saudi Arabia command perhaps the world’s highest government take – the share of project value that goes to the state – given the size of the country’s reserves and the low production cost.

The result would be regular payments made by the international companies over the lifetime of projects. On top of that, the companies would have to meet local content rules such as job creation and training at their own expense. This approach would seem to be more in line with Vision 2030’s emphasis on promoting the private sector and improving efficiency – the latter typically an outcome of a competitive market structure.

The Saudi Aramco IPO is scheduled for 2017-18 on Tadawul, the Saudi stock exchange. As much as five percent of the company will be offered to domestic and foreign investors. According to the newly appointed oil minister, Khalid Al-Falih, a former chief executive officer of Aramco, the listing could result in a market valuation of US $2 trillion for the company, equivalent to almost 11 percent of the GDP of the United States.

The reliability of this estimate has been disputed because little has been disclosed on the company’s inner workings. Al-Falih’s comment that the Saudi government will make sovereign decisions on production and capacity even after the IPO has created unease among analysts, as this could compromise the interests of minority shareholders and depress Saudi Aramco’s market valuation.

Wealth fund

The radical transformation of the Saudi Public Investment Fund (PIF) is another interesting aspect of the reforms.

Unlike its neighbors in the Gulf Cooperation Council, Saudi Arabia does not have a sovereign wealth fund (SWF) that invests oil income for future generations. Only two years ago, Saudi Finance Minister Ibrahim al-Assaf said that the kingdom did not need such a fund. However, one of Vision 2030’s key recommendations is to establish a SWF that might ultimately eclipse the Norwegian Pension Fund Global, currently the world’s largest.

The PIF is not a new entity. It was established in 1971 with a mandate to finance projects in Saudi Arabia through loans or guarantees, as well as by allocations of public funds. According to Vision 2030, the PIF will be transformed into a vehicle for long-term saving and development.

The government’s interest in Saudi Aramco will be transferred to the fund, which will also receive proceeds and dividends from the company’s IPO that would then be invested in non-oil assets. These operations are expected to increase the PIF’s assets from 600 billion riyals to more than 7 trillion riyals ($1.87 trillion), including both domestic and international holdings. Such a portfolio may not be ideal, as investing in local assets will limit diversification and expose the fund to domestic risks – a departure from the usual SWF practice of shielding oil revenue.

Cynical take

Although it favors economic diversification, the IMF acknowledges that “the transformation of oil-exporting economies is no easy task and will be a long-term project. It will require a sustained push for reforms and well-thought-out communications.” In Saudi Arabia, any judgment on whether these prerequisites have been met is still premature.

There has been no shortage of media cynicism about Saudi Arabia’s capacity to follow such an ambitious agenda. The kingdom has a long history of setting ambitious economic goals that have fallen short in implementation. For example, despite regular attempts to control spending, budget overruns have been systematic. This is not limited to Saudi Arabia; the diversification strategy has yielded meager results across the region.

Clarification is still needed in many areas. For instance, while the NTP refers to an income tax on foreigners, the finance minister has stated that the residents’ tax is a only a proposal: “nothing has been approved yet and it will be examined.” Expatriates working in Saudi Arabia have other reasons for concern besides the potential income tax. As Deputy Crown Prince Mohammed bin Salman remarked when asked about creating jobs for young Saudis: “I have reserves now, 10 million jobs that are being occupied by non-Saudi employees that I can resort to at any time of my choosing.” At the same time, the reform agenda allows the quota of foreigners to be expanded for a fee.

In order to encourage the development of the private sector, particularly small and medium-sized companies, Saudi Arabia will have to improve the quality of its regulatory environment – a task that is long overdue. One of Vision 2030’s goals is to improve the kingdom’s ranking in the World Bank’s Ease of Doing Business index to 20 from the current 89, which puts Saudi Arabia ahead of Ukraine but behind Guatemala (81), the United Arab Emirates (31), Bahrain (65), Qatar (68) and Oman (70).

These are only some of the issues in Vision 2030 that require determined follow-through; the list is much longer. But the prospects for successful implementation can only be assessed when the remaining executive programs are published.

Oil policy

The NTP says existing oil production capacity should be maintained at 12.5 million barrels a day (Mb/d), but does not indicate actual output levels.

Saudi Arabia responded to the fall in oil prices in mid-2014 by raising production, which recently has been hovering around 10.2 Mb/d. Saudi Aramco CEO Amin Nasser has raised the possibility of another production increase in 2016.

There seems to be a genuine belief in Riyadh that low oil prices provide the right conditions for the government to pursue its reform agenda. Speaking about oil prices, Prince Mohammed said that “this battle is not my battle. It’s the battle of others who are suffering from low oil prices.” Oil Minister Al-Falih has argued that cheap oil supports reforms and facilitates the restructuring of the economy.

Saudi Arabia will stick to its recent stance of refraining from any production freeze, let alone cuts, unless all other OPEC members come on board. Until then, Riyadh appears content to let market forces shape the oil price.

- Half of Saudi Arabia’s population is aged under 15

- In 2015, the government introduced a 50% increase in water tariffs for governmental and commercial entities and raised fuel prices

- The Saudi budget deficit amounted to $106.3bn in 2015. The government drew down its deposits at the Saudi Arabian Monetary Agency by $106.7bn and issued $25bn of new debt (IMF, 2016)

- The NTP forecasts an increase in public debt to 30% of GDP in 2030 from the current 7.7%, even as the kingdom’s credit rating improves two notches to Aa2 from A1 (Moody’s)

- Female participation in the workforce is set to increase to 28% from 23%

- Saudi Aramco is the world’s fourth largest refiner and the owner of the largest oil reserves (in excess of 280bn barrels)

- The Saudi stock market was opened to foreign investors in June 2015

The article was first published on Geopolitical intelligence Services