Dr Carole Nakhle

After a decade of rapidly growing production, Australia now competes closely with Qatar to be the world’s largest exporter of liquefied natural gas (LNG). This is more remarkable given that the Gulf state’s known reserves are 10 times larger than those of Australia, which has only the world’s 13th-largest proven natural gas reserves (2.4 trillion cubic meters, or 1.3 percent of global reserves).

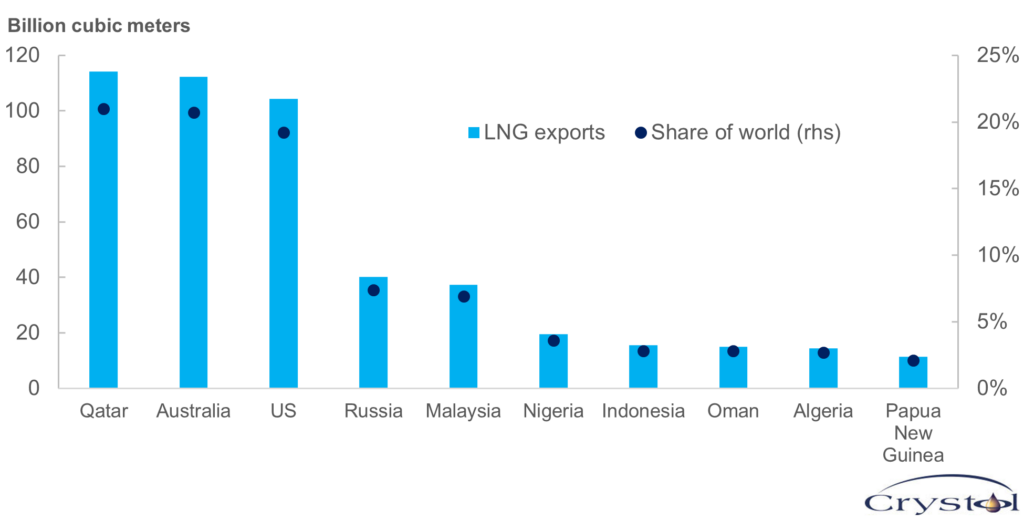

Together with the United States, which sits on the fifth-largest proven reserves, these three giants accounted for 61 percent of global LNG trade in 2022. Other exporters have much smaller shares of the market; Russia, the fourth-largest LNG exporter, has less than half the market share of each of the top three.

However, unlike Qatar and the U.S., which have more diversified markets, Australia is highly reliant on Asia, which absorbed nearly all its exports in 2022. Four Asian countries – China, Japan and South Korea (the world’s three largest LNG importers), plus Taiwan – accounted for 92 percent of Australia’s LNG exports last year. Its proximity to the Asia-Pacific region gives Australia lower transport costs than competitors, making for a natural advantage. The Asian continent is also expected to be the main center of global growth for gas demand in the coming years.

But there are downsides to this dependence. Just as consumers try to secure supply by diversifying their sources, producers can secure demand through a diversification of markets, something that Australia clearly lacks. Moreover, Asia is attractive to Australia’s competitors – not only Qatar and the U.S. but also Russia, which is aggressively looking east and boosting LNG exports to compensate for lost European market share following its invasion of Ukraine.

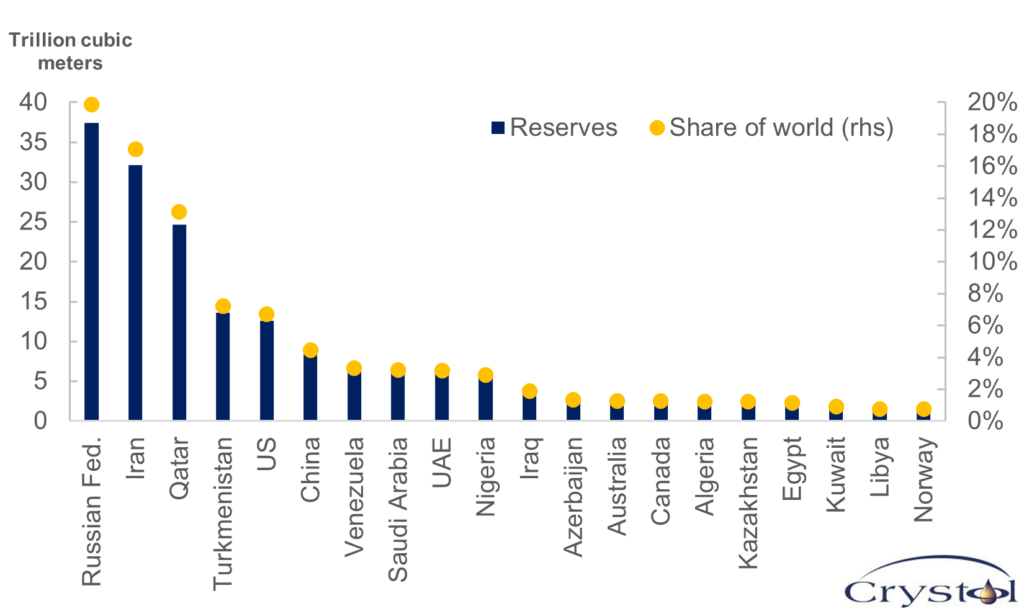

Proved natural gas reserves

Source: Energy Institute

Finally, Australia’s LNG outlook is not as rosy as in the past. While major exporters have announced significant expansion plans, Australia has seen only one LNG project reach a final investment decision since 2012 (Woodside’s Scarborough, in 2021). This has led the government to warn that, without further investment in new LNG trains and gas exploration and production infrastructure, Australia may lose its position as a major LNG exporter.

Rapid ascent

Until the late 1980s, Australia’s gas production was consumed locally. The discovery in the 1970s of offshore giant gas fields in the North West Shelf of the country boosted production in the following years. As production growth exceeded that of local consumption, Australia began selling gas abroad, shipping the first exports in 1989 upon the completion of its first LNG plant, in the North West Shelf.

The growth of the LNG market gained momentum in the 1990s, driven especially by increasing demand from Asia. Several new LNG projects were subsequently launched around the world, including in Australia, which increased LNG exports by nearly 1,000 percent between 2002 and 2022. Last year, exports accounted for 73 percent of the country’s production, nearly all headed to Asian markets.

This dependence cuts both ways. Australia is the largest LNG supplier to Japan (accounting for 43 percent of the country’s imports), Taiwan (37 percent), China (35 percent) and South Korea (25 percent). Typically, Australian gas is sold in Asian markets under long-term contracts.

New markets

An official paper published by the Australian Department of Industry, Science, Energy and Resources identified 11 markets as the best opportunities for LNG trade through 2050. Beyond its four existing main partners, this included seven emerging regional markets: India, Indonesia, Bangladesh, Thailand, Malaysia, Vietnam and the Philippines. The agency recommended that Canberra maintain its engagement with the former group and develop trade with the emerging markets.

The paper also found opportunities in Europe for uncontracted gas as the continent seeks to diversify its supplies, albeit to a smaller extent. Geographically, Australian exports will benefit from a focus on Asia, a premium market with significant demand potential for years to come.

Top LNG exporters, 2022

Data source: Energy Institute

The Asian natural gas market is one of the fastest growing in the world, having expanded at an average rate of 3.2 percent per year between 2012 and 2022. In contrast, Europe, which is the second-largest importing market, contracted by 1.3 percent over the same period. The key drivers of natural gas demand in Asia include rapid urbanization, as well as efforts to reduce air pollution and greenhouse gas emissions (largely because of the dominance of coal in the region). Coal makes up more than 47 percent of the primary energy mix and 56 percent of the electricity mix in Asia-Pacific. A shift to a cleaner fuel, primarily natural gas, can significantly improve the region’s environmental footprint.

China plays a central role in regional and global gas markets, consuming more than 380 billion cubic meters (bcm) of gas in 2022. This was more than the European Union’s total consumption that year (343 bcm), even though natural gas only accounts for under 9 percent of China’s energy mix, compared to 21 percent in the EU.

However, the key to ensuring security of demand for any exporter is through market diversification. Beijing’s ban on Australian coal in 2020 over diplomatic tensions illustrates the dangers of relying on any one market. The Australian government’s effort to develop new markets is one way to diversify the local industry’s portfolio and protect its contributions to the national economy.

Qatar, the U.S. and Russia

The growing gas markets of Asia are attracting producers beyond Australia – including the U.S., Qatar and increasingly Russia, among others.

The Asia-Pacific is already the most important market for Qatari LNG, accounting for more than 71 percent of its exports (followed by Europe, which captures 28 percent). Based on reserve size and production cost, where it has a clear advantage over the closest competitors, Qatar is well placed to benefit from any growth in LNG demand in both Asia and Europe. Moreover, its geographical location enables the Gulf state to pursue arbitrage between those two regions.

Although Qatar temporarily lost its spot as the top LNG exporter to Australia in 2020 and 2021, this was largely due to a self-imposed moratorium on further exploration and development of its super giant North Field, announced in 2005. The moratorium was extended several times before finally being lifted in 2017. That decision was driven by increased competition in the global market, owing to the growing presence of the U.S. and Australia as well as expected growth in gas demand in Asia-Pacific. Qatar’s North Field expansion is set to see one of the most significant developments in the industry, significantly boosting supplies in the coming years.

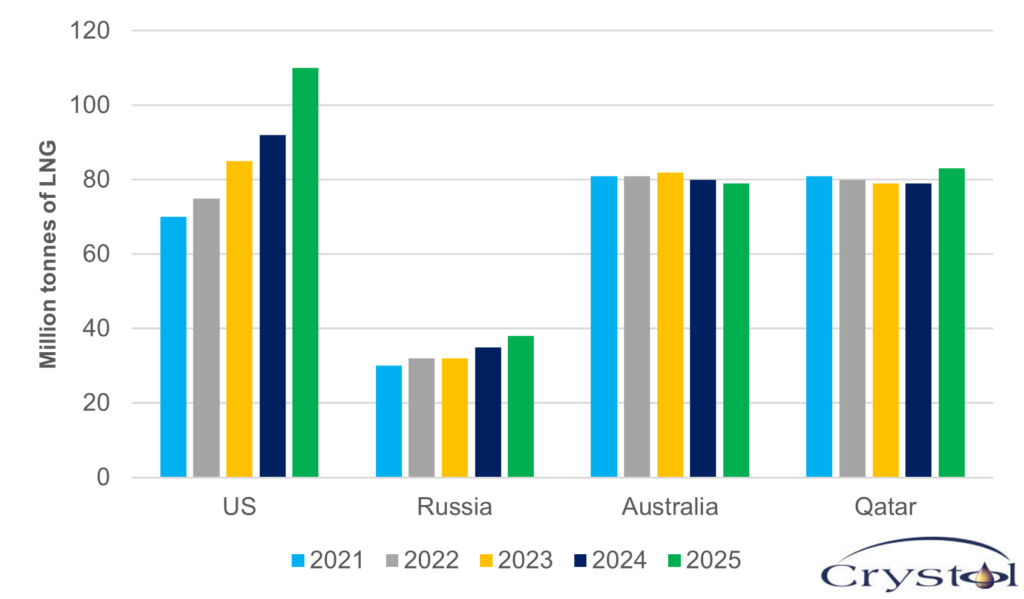

Global LNG supply forecasts, 2021-2025

Data source: Australian Department of Industry, Science and Resources

After being a net gas importer for years, the U.S. has made a remarkable turnaround to become the third-largest LNG exporter. Over the next five years, it has a good chance to become the world’s biggest exporter, supported by a strong wave of projects coming online by 2026.

One characteristic of American LNG is destination flexibility: cargoes are free to flow to the importing markets that offer the highest margin. For instance, over the last few years, the U.S. has focused on Asia-Pacific, which absorbed nearly half of American LNG exports in 2021, followed by Europe (at 32 percent). However, in 2022, as Europe looked for alternative supplies to Russian gas, it captured nearly 70 percent of U.S. LNG exports, compared to 23 percent from Asia. In both regions, the U.S. enjoys a diverse customer base.

Then there is Russia. Long before its full-scale invasion of Ukraine, Moscow was preparing for a shift in the geography of energy demand toward Asia, as well as a slowdown in growth in the European market – a trend that has accelerated since 2014 (following the annexation of Crimea and the subsequent imposition of Western sanctions). Russia’s “Energy Strategy to 2035” forecasts significant growth for both gas production and exports, both of pipeline gas and even more so LNG, with Asia absorbing larger shares. The war in Ukraine has accelerated Russia’s turn to Asia, with China as the main target.

As Canberra has warned: “The opportunity for Australia is huge, but so is the appetite of our competitors to snatch it from us.”

Domestic dynamics

Several domestic developments have raised concerns about the ability of Australia to expand its LNG exports to meet potential demand growth.

In 2017, the Australian Domestic Gas Security Mechanism (ADGSM) became effective. The policy aims to guarantee a sufficient supply of natural gas to meet domestic needs, limiting LNG exports from certain plants if necessary. In 2022, the government said it expects a tight domestic market through 2030 – increasing the risk of domestic gas shortages – and accordingly announced that the decision to activate the ADGSM can be made on a quarterly basis. Although authorities stated that any diversions of exports to the domestic market would apply to uncontracted gas, any such move would limit Australia’s export potential plans.

Meanwhile, there is ongoing criticism of Australia’s heavy reliance on coal, which meets 48 percent of the country’s electricity needs. A switch to gas, which is a cleaner fossil fuel, would support efforts to reduce greenhouse gas emissions. But it would also mean greater domestic LNG demand and subsequent erosion of exports unless production capacity is also expanded.

In July 2023, a new environmental rule began requiring new LNG facilities to be carbon- neutral on their first day of operations. The measure has worried Australia’s top customer, Japan, which fears delays in bringing new LNG supplies onstream.

On top of these concerns is a fundamental deficit of investment. Between 2001 and 2021, Australia’s LNG exports grew more than tenfold, as many projects were commissioned. This growth, however, is expected to decelerate. The Australian government has warned that the country is lagging behind its competitors in terms of new investment in the sector.

Scenarios

The outlook for Australian LNG is best summarized in a recent government paper on the industry’s mid-term outlook. “Despite the favorable environment for LNG producers, the outlook for Australia is mixed,” it found. “Australian LNG exports are forecast to fall marginally, as existing facilities face difficulties backfilling their operations with gas from new reserves. At the same time, investment in offshore exploration remains low despite high commodity prices, which could impact Australian gas production beyond the outlook period.”

Without accelerated investment in both the exploration and production of gas, as well as in LNG infrastructure, Australia’s golden age of gas will soon come to an end.

Related Analysis

“Increasing pressure on Russia’s oil industry“, Dr Carole Nakhle, Apr 2023

Related Comments

“Saudi Arabia Voluntary Output Cut“, Dr Carole Nakhle, Jun 2023

“OPEC+ makes shock million barrel cut“, Dr Carole Nakhle, Apr 2023