Lord Howell

Radical changes continue to sweep through global energy markets, bringing with them big new opportunities, as well as serious dangers. New technology, geopolitical turmoil and market power are the drivers. As the full implications sink in, policy makers, both in Europe and elsewhere, will struggle to respond and reconcile cost, security and environmental aims – with limited success.

RADICAL changes are under way in the world energy landscape, presenting big new dangers and big new opportunities.

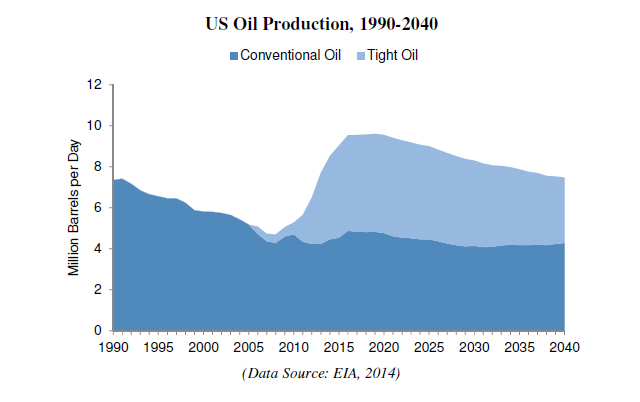

At the global level the impetus of energy demand has already shifted from west to east, while the emerging pattern of energy supplies is moving the other way, as America switches round from being the thirstiest oil and gas importer to the biggest home producer and, just ahead, potential exporter. American markets for Middle East oil have shrivelled, while China’s imports grow and Japan continues, at least temporarily, to siphon up large daily oil and gas imports to fill the gap left by the continuing shut-down in its nuclear power, previously 40 per cent of its electric power source.

Meanwhile, although Europe’s oil import demand, like America’s, is shrinking its gas needs are rising and fears of Russian intentions are casting a deep shadow over its supply security. Decarbonisation aims are clashing increasingly with both cost and security concerns and European energy policy is stumbling towards major revision. Perverse consequences of current policy are forcing a re-think on several fronts, as coal burning rises, coal imports soar – both from America and from Czech lignite sources – emissions rise instead of falling, renewables subsidies become too much for cash-starved Governments to bear and high energy prices undermine European industrial competitiveness and deter new investment – a point which German business leaders make with increasing frequency.

Hostility in many European states to unconventional gas exploitation – fracking – bars one further way forward for Europe. France is opposed outright, Germany and Austria are reluctant while in Britain, despite Government’s efforts to encourage fracking little is happening. Obstacles are also strewn across the nuclear power path with Mrs Merkel’s decision to close down Germany’s nuclear power sector, extensive budget and timing overruns with EDF’s new projects in Finland and in France and the UK’s highly controversial commitment to a new plant at Hinckley Point being criticised from many sides. Consumers are worried at the high ‘strike price’ with which they are stuck for 35 years, while technicians note that no single model of the proposed EPR has yet been in operation.

For the Middle East oil producers the impact of these various developments is especially challenging. Regarded for the last century, along with North Africa, as the world’s major and strategic oil source, possessor of two thirds of proven oil reserves and dominant oil market force, the question now is how Middle East states will respond as political turmoil engulfs the region.

This might have been expected to send crude prices climbing but instead they have fallen back, indicating that new market determinants are beginning to operate.

These could work the opposite way to past patterns. Middle East producers could now find themselves facing entirely new conditions and having to deal with new and very different customers from the past.

Chinese demand will stay high but is not growing as fast as hopefully expected by oil producers and Japan will get its nuclear sector re-started, at least in part, before long. Western markets will stay flat or, in the American case shrink sharply, a major switch to lower carbon gas will accelerate and shale potential almost everywhere could move towards greater realisation.

Meanwhile new technology is bringing the price of many, although not all, alternative renewable energy resources gradually down, especially solar power, while energy use efficiency has made significant strides at every point in the supply chain, from production to the final consumer and all along the generating, transmission and distribution systems.

Transport, supposedly the one safe area for oil sales, is also being subjected to inroads from gas and gas-powered electricity.

Over-hasty investors in renewable energy production, putting their faith in unending subsidies, are being disappointed, as they were bound to be, but domestic consumers are starting to see real cost advantage in greener alternatives and more efficient consumption.

All this creates a new and unfamiliar market scene in which oil and gas supply will remain plentiful and net demand growth will be moderate – sure conditions for softer prices and more hesitant investment commitments. Saudi-Arabia’s power as swing producer will remain by virtue of the sheer size of its production capacity, but the ‘swing’ instrument will prove more difficult to use as other oil, gas and non-fossil energy resources kick in.

A further twist will come from the rapid rise of domestic oil consumption in the Gulf States. On estimate (from Chatham House in London) suggests that by 2030 Saudi-Arabia will consume most of its production at home and have precious little to export.

The biggest unsolved challenge for world power supplies remains the 1.3 billion people who have no electricity access. Solar technology may be the most hopeful path for power-deprived communities, at least at the domestic and village level.

But for sustained economic development, low-income countries need affordable (in other words cheap) and reliable high voltage current. Continuing to burn costly diesel is no longer an option. It remains to be seen how far coal is going to continue as the unavoidable and least expensive source of power generation, as is clearly the case on the Indian sub-continent, and still also in China, and how far gas, mainly in LNG form, can replace coal and provide a significantly lower carbon source for developing societies.

A positive aspect of this scene is that many poorer economies, including those in Africa, are finding new ways of commercially exploiting their own resources, including shale. A less positive aspect is that coal still remains the largest source of electric power across the globe.

The full and enormous implications of what is occurring have been slow to dawn on energy companies, as well as policy makers and international institutions.

In essence the energy significance of the Middle East has begun to decline – at least from the Western point of view. At the same time the shift in energy resource patterns has accelerated, opening up major new supply potential not only in America and Australia but in many parts of the so-called developing world. A new energy balance world-wide is emerging, which meets some, but by no means all, of the current climate concerns.

As always, market forces and technology will prevail and policy and politics will in the end adjust.