Dr Carole Nakhle

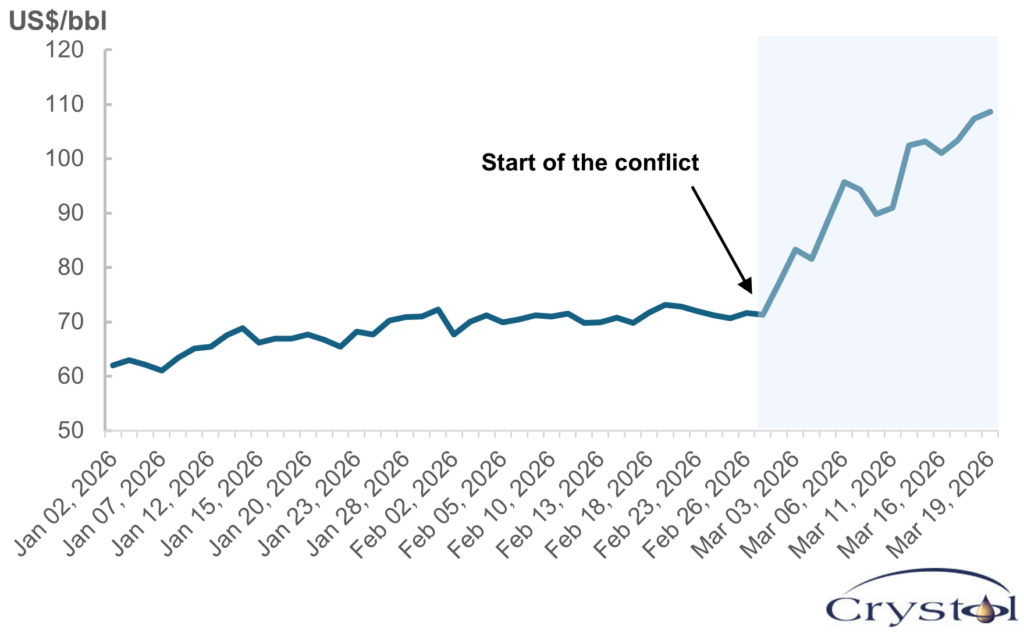

The latest escalation in the Middle East came as a shock to global oil markets. Tensions had been rising, particularly following the largest United States military buildup in the region since the first Gulf War. Markets were increasingly factoring in the possibility of military action, albeit largely assuming a limited event.

What followed went well beyond that. Iran’s response, which included attacks on energy infrastructure throughout the region, as well as the effective disruption of traffic through the Strait of Hormuz, transformed the situation abruptly.

The Strait of Hormuz is the world’s most important oil chokepoint, through which around a fifth of global trade passes. When its flows are disrupted, the consequences are felt immediately. As traffic through the strait came to a standstill, several Arab oil producers were forced to temporarily halt part of their production as storage capacity began to fill. Close to 20 percent of global oil trade was suddenly disrupted, while parts of the region’s energy infrastructure also came under pressure.

Daily spot price of Brent crude oil

Source: Energy Information Administration (EIA), Bloomberg

Against this backdrop, oil prices rose sharply and remain under upward pressure, especially as the war shows no clear sign of ending. Even more notable, however, is the high level of price volatility. Markets are reacting almost in real time to political statements and signals from the parties involved, moving sharply with each indication of escalation or de-escalation.

Prices have been higher in past crises, and may rise dramatically still. For the time being, prices do not appear fully commensurate with the scale of the disruption – a reminder that even in severe crises, market outcomes are shaped by underlying conditions and available buffers.

What ultimately matters now is not only the trajectory of oil prices, but the broader implications for the region. The war’s more enduring impact will be whether it paves the way to a more stable Middle East or leaves behind a more fragile geopolitical landscape, with significant implications for global oil markets.

The core of the global oil system

It is no exaggeration to say that the global oil market, as we know it today, is built around the Middle East. The region is home to the largest concentration of global proven oil reserves, accounting for almost half. It also provides more than 30 percent of global oil production, exceeding the combined output of regions such as the Commonwealth of Independent States (CIS), Europe, Asia-Pacific and Africa. Several of the world’s largest producers, including Saudi Arabia (the world’s second-largest producer), Iran (fifth), Iraq (sixth), the United Arab Emirates (eighth) and Kuwait (10th), are located in the region. These countries also form the backbone of the Organization of the Petroleum Exporting Countries (OPEC).

More importantly, the Middle East holds most of the world’s spare production capacity, concentrated largely in a small number of Gulf producers, notably Saudi Arabia and the UAE, with more limited volumes in Kuwait. Historically, the region has acted as the system’s primary buffer in times of disruption, serving as the global oil market’s shock absorber.

This time, however, the crisis has affected each of these producers. More than 40 energy sites, including oil refineries, natural gas fields, export infrastructure and other key facilities, have been damaged across nine Middle Eastern countries since the escalation began. Some have been struck repeatedly with both drones and missiles.

But oil supply is not just about production. It also depends on the ability to move barrels to market. A large share of globally traded crude from the region must pass through a single chokepoint: the Strait of Hormuz.

What makes Hormuz unique is the combination of scale and the absence of viable alternatives. On a normal day, around 20 million barrels per day (mb/d) transit the strait, the equivalent of a fifth of global oil consumption. Other major chokepoints, such as the Suez Canal or the Strait of Malacca, also carry significant volumes of trade. But in those locations, rerouting is possible. When a container ship blocked the Suez Canal in 2021, vessels were diverted around the Cape of Good Hope. Similarly, flows through Malacca can be redirected through alternative Indonesian straits, albeit at higher cost and longer transit times. However, for the majority of Gulf producers, there is simply no rerouting option for tankers going through the Strait of Hormuz. Pipelines such as Saudi Arabia’s East-West pipeline, the UAE’s Abu Dhabi-Fujairah line, and Iraq’s export routes to the Mediterranean provide some bypass capacity. However, these routes do not come close to matching the scale handled by the strait.

Even where production capacity remains intact, the inability to export forces producers to curtail their output as storage fills. This has already been observed across parts of the Gulf, where operators have declared force majeure and suspended production, as they can no longer move crude to international markets following the disruption of flows through the Strait of Hormuz.

Policy response in the aftermath of the disruption

Governments and international institutions have moved rapidly to deploy a wide range of measures aimed at stabilizing markets and containing price pressures.

The most immediate response has been the mobilization of strategic petroleum reserves. The U.S., along with other International Energy Agency (IEA) member countries, has initiated the largest coordinated release of emergency stocks in history, with a total of around 400 million barrels agreed across member countries. By comparison, previous coordinated releases, such as in 2011 during the Libya crisis and in 2022 following Russia’s invasion of Ukraine, amounted to roughly 60 million and 180 million barrels respectively.

Efforts have also focused on restoring the flow of oil through the Strait of Hormuz. The U.S. has taken a leading role, proposing additional insurance mechanisms for tankers, deploying naval escorts and calling for broader international support, including from NATO allies.

A key element of this effort has been the attempt to address the surge in war-risk premiums, which have risen sharply as insurers reassess the risks of transiting through Hormuz, with some withdrawing war-risk coverage altogether. Without such cover, many shipowners are unwilling to sail through the strait, effectively halting trade regardless of available supply.

In response, the White House has suggested government-backed insurance and guarantees to cover war-risk exposure for tankers transiting the strait. However, details remain limited, and the impact of this proposed arrangement has been constrained by persistently high risks and operational challenges that continue to deter shipping.

Military measures have also been considered, including escorted convoys through the strait, drawing on precedents such as Operation Earnest Will in the late 1980s, when the U.S. reflagged and escorted Kuwaiti tankers during the Iran-Iraq war. That operation helped ensure that oil continued to flow, but under conditions of heightened risk, with tankers still subject to mines and attacks.

Today, the nature of the threat has evolved. The increased use of drones and precision strikes extends risks beyond what naval escorts alone can address. Shipping decisions still depend on commercial costs and insurance coverage, which military protection cannot fully address. In addition, coordination remains limited, and NATO has not engaged with the conflict as a formal alliance.

Another effort that has been implemented is relaxing or suspending sanctions enforcement on key producers – including Russia and, notably, Iran – to allow additional barrels through. This has allowed previously sanctioned Iranian cargoes, already loaded and stranded at sea since the war began, to find buyers.

Demand-side measures have also been introduced, particularly in Asia. Governments have encouraged reduced energy consumption through policies such as remote working – as in Japan and South Korea, and transport restrictions, including limits on private vehicle use in major cities such as New Delhi. The IEA has also issued recommendations outlining practical steps to curb oil demand in the short term, ranging from behavioral changes to transport-related adjustments.

The intensity of the response has been amplified by a broader crisis narrative in the media and institutional debate. However, this sense of urgency is not uniform across regions. In Europe, for instance, reactions have been more measured than during the energy crisis of 2022, probably reflecting both improved preparedness and a different perception of risk.

A major impact on oil supply

The scale of disruption, the concentration of supply affected and the strategic importance of the Middle East all point to a high-risk environment. Moreover, the possibility of further escalation cannot be ruled out. The scale of this disruption is unprecedented in volumetric terms. Estimates suggest that between 10 and 15 mb/d of supply have been affected, making this the largest supply shock in the history of the global oil market.

The narrative surrounding this disruption has at times moved ahead of the underlying reality. This is not unusual in periods of heightened geopolitical tension, where uncertainty itself becomes a driver of market sentiment.

It is true that the loss of supply is unprecedented. However, such comparisons can be misleading if taken in isolation. The global oil market today is larger than ever, with total supply exceeding 104 mb/d. In that context, even a disruption of this magnitude, while considerable, represents a smaller share of total supply than comparable shocks in earlier decades. Oil prices, while elevated, remain around $100 per barrel, well below the peaks observed during previous crises when measured in real terms. Smaller disruptions in the past have led to significantly higher price levels once adjusted for inflation.

This is not to suggest that the current situation is benign, nor that the risks are limited. On the contrary, the outlook remains uncertain, and further escalation could materially alter market dynamics. Still, the current price response, while significant, is not exceptional by historical standards. This partly reflects the nature of the disruption: Much of the supply loss is driven by logistical constraints that prevent oil from reaching markets, rather than permanent damage to infrastructure. The market therefore remains, at least for now, more resilient than predominant narratives suggest.

Scenarios

Any outlook for oil markets remains contingent on the trajectory of the conflict itself, which is highly uncertain. Rather than attempting to predict its course, it is more useful to consider how the region’s role as a key supplier may evolve.

Most likely: Middle East remains a major oil supplier

The most likely outcome is one in which the region remains a central supplier of oil, but under continued uncertainty.

Much of the current damage, while significant, is likely to be reversible. As facilities are repaired and flows resume, lost production could return within months rather than years. Production capacity largely remains intact, and flows through the Strait of Hormuz resume, even if unevenly.

In the absence of a clear and lasting resolution, a risk premium may persist, but it is likely to fluctuate rather than become entrenched. Prices remain volatile, reacting to developments on the ground, but do not necessarily move to structurally higher levels. At the same time, the region’s dependence on the Strait of Hormuz is brought into sharper focus, potentially accelerating efforts to expand alternative export routes, even if these cannot fully replace it. Oil markets continue to function, but remain sensitive to geopolitical developments as long as uncertainty persists.

Less likely: A lasting shift away from Middle East

A less likely scenario would involve a deeper and more lasting shift in how global oil supply is structured.

In this case, repeated disruptions lead to a reassessment of the region’s reliability as a supplier. Ongoing instability could delay investment, disrupt future supply growth and weaken confidence in the region’s ability to act as the system’s primary buffer. Prices could experience sharper and more frequent spikes, reflecting tighter conditions and heightened risk.

The more significant shift would be structural. Investment may increasingly flow toward alternative sources outside the Middle East, while consuming countries accelerate efforts to diversify supply and reduce exposure to chokepoints such as Hormuz. At the same time, coordination among producers could become more difficult, weakening the effectiveness of collective frameworks such as OPEC.

Related Analysis

“Global oil market dynamics after U.S. intervention in Venezuela“, Dr Carole Nakhle, Jan 2026

Related Comments

“The Saudi oil pipeline the world didn’t know it needed“, Dr Carole Nakhle, Mar 2026

“US eases sanctions on Russian oil amid energy crisis sparked by Iran conflict“, Christof Rühl, Mar 2026

“War puts key Iranian oil terminals at risk“, Dr Carole Nakhle, Mar 2026