Dr Carole Nakhle

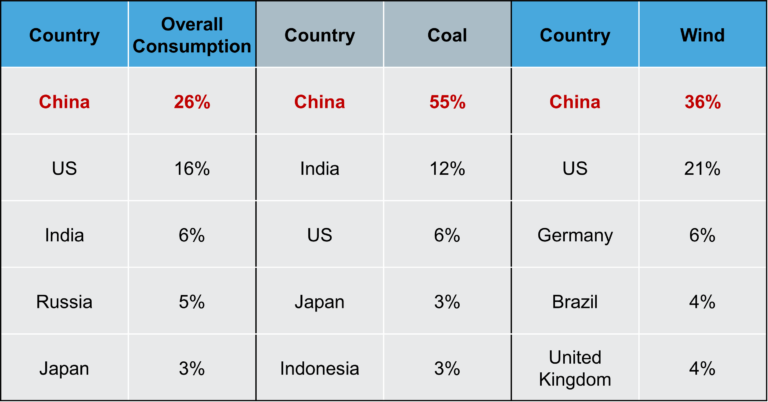

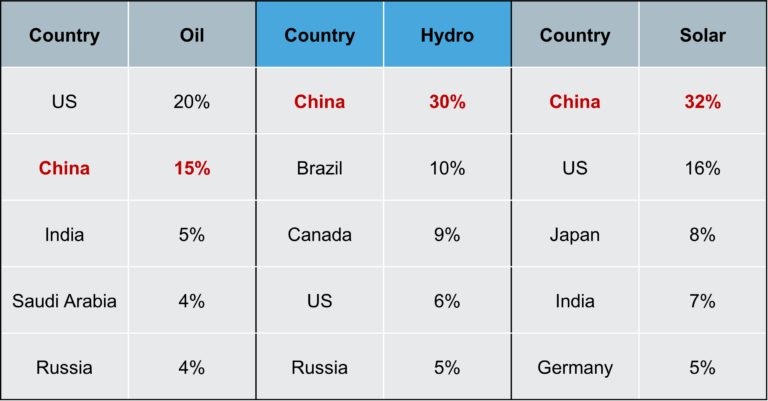

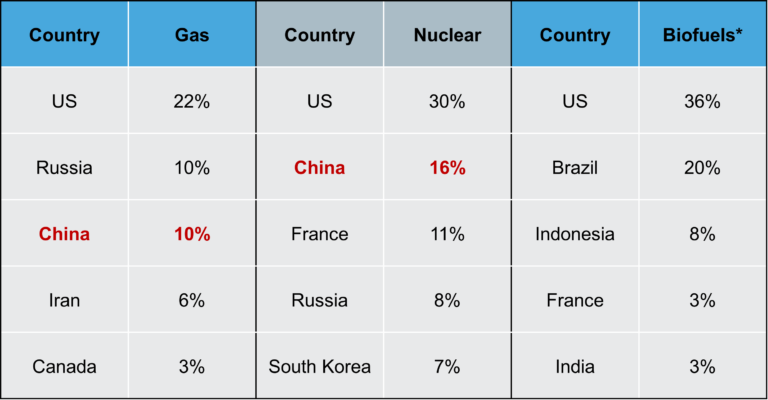

China is the world’s biggest energy consumer and importer, as well as a major producer of energy and other related commodities. Its influence on global energy markets and trade is immense. The Asian powerhouse accounted for more than a quarter of global consumption in 2022. It also consistently ranks among the top three consumers of oil, gas, coal, nuclear, hydro, wind and solar power. And it is a world leader in the production of electric vehicles (EVs), as well as the largest market for such cars.

Over the past decade, the pace of energy consumption in China has significantly outstripped the global norm. Although it is a major producer (the world’s largest in coal, fourth largest in natural gas and sixth in oil), Chinese growth in local consumption outpaced domestic supply – turning the country into a major commodities importer, with significant consequences on global trade. Oil, gas and coal imports to China account for around 85 percent, 40 percent and 7 percent of the country’s domestic consumption, respectively; and about 18 percent, 16 percent and 18 percent of the global trade of these commodities.

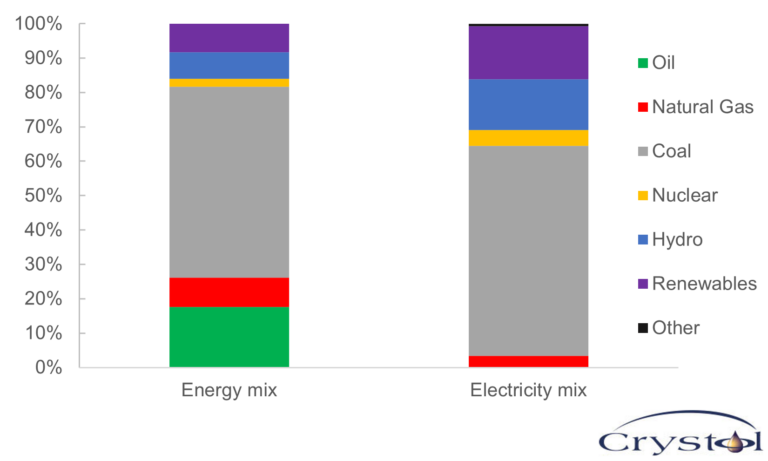

China’s mixes of electricity consumption and overall energy use are both dominated by coal, which is by far the worst emitter of greenhouse gases. This makes China the largest emitter of carbon dioxide, accounting for more than 37 percent of the world’s total and more than double the next-worst emitter, the United States (14 percent). But it is not only through its CO2 emissions that China affects the energy transition. An important producer of renewable energy, the country is also a major supplier and refiner of many metals and minerals necessary to manufacture green technologies, from battery storage to solar panels.

Russia’s war on Ukraine has further amplified the Chinese role in redrawing global energy trade flows, particularly in oil and gas, with repercussions on prices and competition between markets and suppliers.

Top energy consumers by fuel type and share of world consumption

Source: Energy Institute *China ranks 7th (accounting for about 2% of biofuel consumption), with Germany 6th

Post-Covid China and war in Europe

China was the first country to close its borders when the Covid-19 pandemic hit, after serving as its ground zero. It was also the last to reopen, after pursuing a zero-Covid policy for several years. That approach was abandoned in December 2022, following a massive toll on the economy and society and a failure to achieve its goals. The policy also affected the country’s demand for energy commodities, with spillover effects on global trade and prices.

In 2020 and 2021, Chinese oil demand grew by only 1 percent and 3 percent, respectively, whereas in 2022 demand shrank by 4 percent to reach 14.3 million barrels per day. This is a significant slowdown given that its oil demand grew at an average of nearly 6 percent annually between 2009 and 2019. Similarly, China’s gas consumption decreased by around 1 percent in 2022 – the weakest annual growth since the early 1990s. The country subsequently lost its top rank as the world’s largest buyer of liquefied natural gas (LNG) to Japan.

This slowdown was a boon to consumers in the rest of the world (and particularly in Europe) as it helped ease pressure on prices, especially following the outbreak of war in Ukraine and subsequent supply disruptions. Had China’s energy demand been growing at the levels prevailing before the pandemic, Europe would have faced much higher LNG prices, being forced to outbid its tough Asian competitor.

China’s reopening in early 2023 has led many observers to fear significant upward pressure on energy prices, given expectations of a strong recovery in oil and gas demand. For instance, the International Energy Agency (IEA) expects China to account for 70 percent of the year’s 2.2 million barrels per day of growth in oil demand, driven by transportation fuels (such as gasoline and jet fuel) and robust support from the petrochemicals sector. Earlier in the year, Goldman Sachs forecasted that the Chinese market would boost Brent by roughly $15 per barrel. The IEA also sees Chinese gas demand growing by 6.6 percent in 2023 – at a time when global demand is otherwise expected to stall – and that China will be the single largest contributor to global gas consumption growth by 2025.

Market share

For energy exporters, even during a slowdown, China remains a sizable market, accounting for a significant proportion of the total Asia-Pacific market, which is the largest importing region for oil and gas and well ahead of Europe.

The Chinese oil market uses 14.3 million barrels per day – nearly equivalent to the oil consumption of the entire European continent in 2022 and accounting for 40 percent of Asia-Pacific demand. Its gas market comes to about 376 billion cubic meters (bcm), which equals nearly three quarters of the European market in 2022 and accounts for 41 percent of regional demand.

Its growth has also outshined that of other big competitors. For instance, over the last decade, average Chinese oil and gas demand growth was 3.6 percent and 9.6 percent per year, compared to annual contractions of 0.4 percent and 1.1 percent in the European Union. The potential for natural gas is notable, as China is already the world’s third-largest gas-consuming country (after the U.S. and Russia). This is true even as the share of natural gas in China’s energy mix remains very low compared to other markets, and with Beijing looking for alternatives to coal to reduce the country’s carbon footprint.

China’s energy and electricity mixes

Source: Energy Institute

Not surprisingly, China has been the focus of major producers, particularly Russia, which looked at its Asian neighbor as an alternative to the shrinking European market even before the invasion of Ukraine. The war has only accelerated the trend.

Redrawing trade flows

Russia has been gradually expanding into Asia and particularly China. The 2011 completion of the Eastern Siberia-Pacific Ocean oil pipeline (ESPO) created a key route for Russian oil to reach consumers in Asia (mainly China, Japan and South Korea), while also allowing Beijing to reduce its exposure to eastern trade choke points, such as the Strait of Taiwan. After the European Union, traditionally Russia’s biggest market, imposed an embargo on all imports of Russian oil by sea, the sanctioned oil – which had been trading at a discount to international prices – found refuge in Asia.

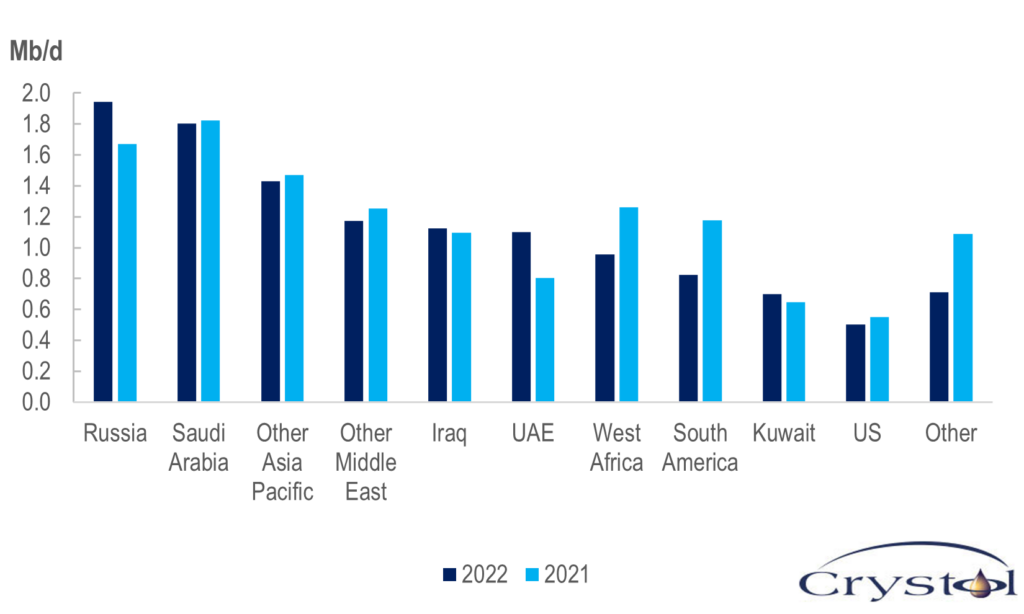

In 2022, Russian oil exports to China grew by 16 percent, with Russia gaining market share primarily at the expense of suppliers in West Africa and South America, and to a lesser extent the U.S. and some Middle Eastern producers (which subsequently redirected some of their oil to Europe). Russia became the biggest oil supplier to China, representing 16 percent of Chinese imports and surpassing Saudi Arabia (15 percent of China’s imports), which was the country’s largest supplier for years. Although Saudi Arabia saw only a small dent in its market share in China, the kingdom has been taking decisive actions to safeguard its long-term position there. In 2022, for instance, Saudi Aramco, the Saudi national oil company, finalized plans to build a $10 billion refinery and petrochemical complex in northeastern China, marking its single largest investment in the country.

At the same time, China – the world’s second-largest oil refiner after the U.S. – has boosted its exports of refined oil products. Beijing has taken advantage of cheap Russian crude feedstock to achieve lucrative margins for domestic refineries while helping to ease pressure on global consumers, especially after Russia announced a “temporary” ban on fuel exports.

Oil suppliers to China

Source: Energy Institute

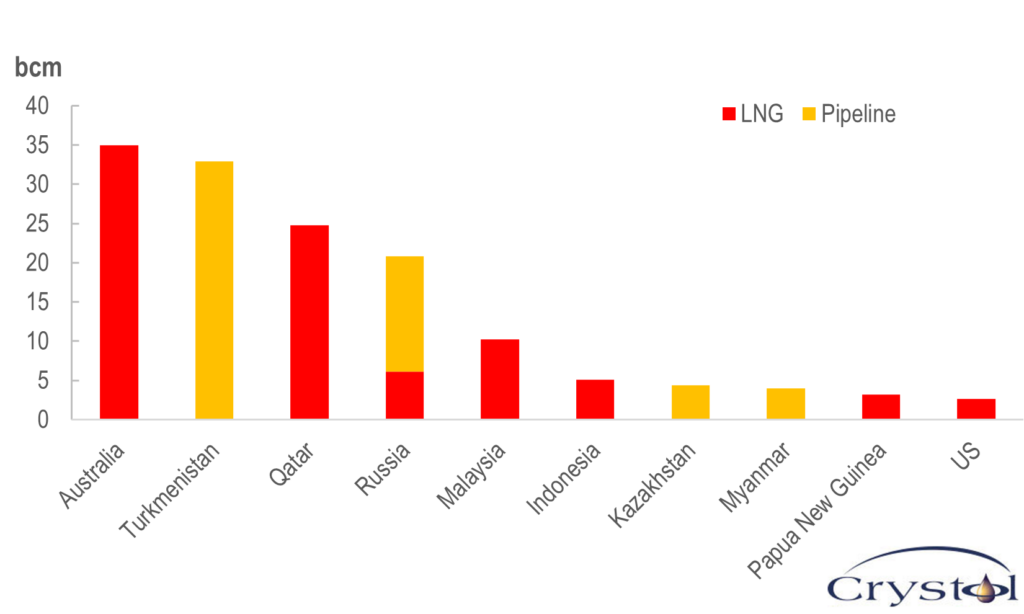

Top gas suppliers to China, 2022

Source: Energy Institute

On the gas front, Australia and Qatar historically dominated LNG trade with China, while Turkmenistan was the largest supplier of pipeline gas to China. Before 2019, Russia supplied up to 3 percent of China’s gas imports, largely via LNG. But that relationship changed with the opening of the Power of Siberia 1 gas pipeline, which had a capacity of 38 bcm in 2019. Russia shifted from being a marginal supplier of gas to China to becoming its fourth-largest supplier, accounting for 8.5 percent of the country’s gas imports. Between 2021 and 2022, Russian gas exports to China increased by more than 50 percent. In contrast, American exports to China dropped by almost 80 percent, heading instead to Europe to fill the gap left by Russia.

Russia’s presence in the Chinese gas market is set to further expand if the Power of Siberia 2 project, a more strategic pipeline with a 50-bcm capacity, is built. If and when that happens, it would give Russia a replacement for its lost gas exports to Europe. However, China’s would-be position as the largest buyer of Russian gas might lead Moscow to offer more concessions to complete the project, and could potentially limit its bargaining power with Beijing.

Another important player seeking to consolidate its presence in China is Qatar. Between 2021 and 2022, the Gulf state doubled both exports to China and the size of its share in China’s gas import mix. The two countries have signed two long-term LNG contracts that would lock in 11 bcm of Qatari gas destined for China every year for the next 27 years.

Security of supply

China’s footprint on global energy markets and trade is notable. It features in the strategy of every large exporter, particularly in oil and gas, since China is expected to be the main growth engine for energy demand in the coming years.

Beijing will continue to skillfully maneuver its relationships with various trade partners to secure its supplies. However, the country is unlikely to overly rely on any single supplier as its energy security objectives focus on having a balanced portfolio of imports. “We will diversify and expand the sources of oil and gas imports and maintain the security of strategic channels,” the government stated in its 14th Five-Year Plan for National Economic and Social Development and Long-Range Objectives for 2035, published in 2021.

Maintaining a diversity of suppliers also gives China greater bargaining power, not only to negotiate favorable deals but also to retain and obtain additional political leverage. It has already made itself indispensable for many partners, including Russia.

Facts & Figures

China facts:

- Between 2012 and 2022, China’s overall energy, oil and gas demand grew at an annual rate of 3.1% (versus 1.4% globally), 4% (versus 0.9% globally), and 9.6% (versus 1.7% globally), respectively (Energy Institute)

- China is the largest producer of 31 metals and minerals and is the world’s largest mining nation (World Mining Data, 2022)

- Transport accounts for the biggest share of Chinese oil demand (48.5%), followed by non-energy use (24.5%) and the industrial sector (14.6%) with minor contributions from the residential, commercial and agricultural sectors (IEA)

- The industrial sector accounts for the largest portion of natural gas consumption (42%), followed by the residential sector (33%), the power sector (17%) and the chemicals sector (8%) (China’s National Energy Administration)

Related Analysis

“China’s energy and climate plans under threat“, Dr Carole Nakhle, Apr 2022

Related Comments

“Will China Controls on Graphite Exports Affect the Energy Sector?“, Dr Carole Nakhle, Oct 2023

“China accounts for 70% of oil demand growth in 2023“, Dr Carole Nakhle, Aug 2023

“The role of China in oil markets“, Dr Carole Nakhle, Jan 2023